IMF Conditionality and Pakistan’s Structural Reform Dilemma in a Fragmented Global Economy

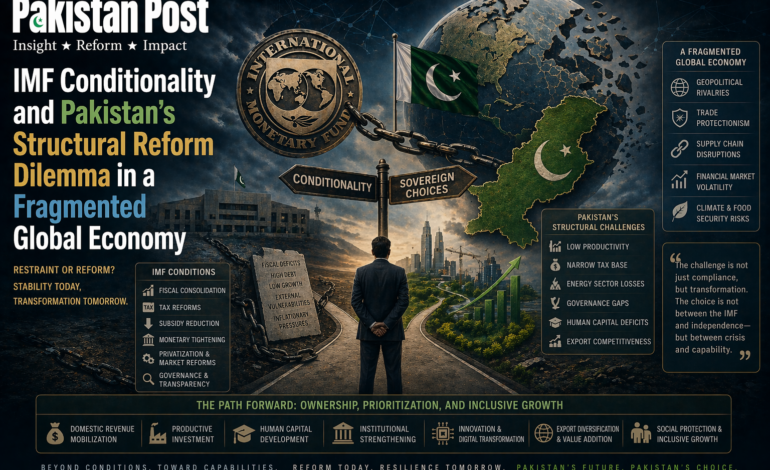

Pakistan’s economic story in recent years has increasingly been written in the language of stabilization, adjustment, and external dependency. At the center of this narrative sits the International Monetary Fund, returning repeatedly as lender of last resort, policy architect, and macroeconomic disciplinarian. Yet beneath the surface of stabilization packages and reform commitments lies a deeper structural dilemma: whether Pakistan is building a self-sustaining economic framework or entrenching a cyclical dependence on external financial support that resets crisis after crisis without resolving its underlying causes.

In its most recent engagements with the IMF, Pakistan has undertaken a familiar set of reforms. These include fiscal consolidation through tax expansion, energy tariff adjustments aimed at reducing circular debt, exchange rate flexibility to correct external imbalances, and efforts to restructure loss-making state-owned enterprises. On paper, the logic is coherent: restore macroeconomic stability, rebuild reserves, and re-anchor investor confidence. In practice, however, the sequencing and political economy of these reforms reveal a far more fragile reality.

Pakistan’s reform trajectory is constrained by a persistent tension between external conditionality and domestic political legitimacy. IMF programs are designed to correct macroeconomic imbalances through front-loaded adjustments, but Pakistan’s political system operates on short electoral cycles, coalition fragility, and entrenched distributional interests. This mismatch produces a recurring pattern: reforms are initiated under crisis pressure, partially implemented under external supervision, and then gradually diluted as political resistance builds or as immediate macroeconomic pressure eases.

Tax reform illustrates this contradiction clearly. Pakistan’s tax-to-GDP ratio remains structurally low compared to regional peers, constrained by a narrow tax base, widespread informality, and politically influential exemptions. IMF-backed programs consistently push for broadening the tax net, increasing compliance, and reducing exemptions in retail, real estate, and agriculture. Yet each attempt faces resistance from powerful domestic constituencies embedded within the political economy. As a result, incremental gains in revenue collection are often offset by administrative inefficiencies and policy reversals, limiting long-term fiscal transformation.

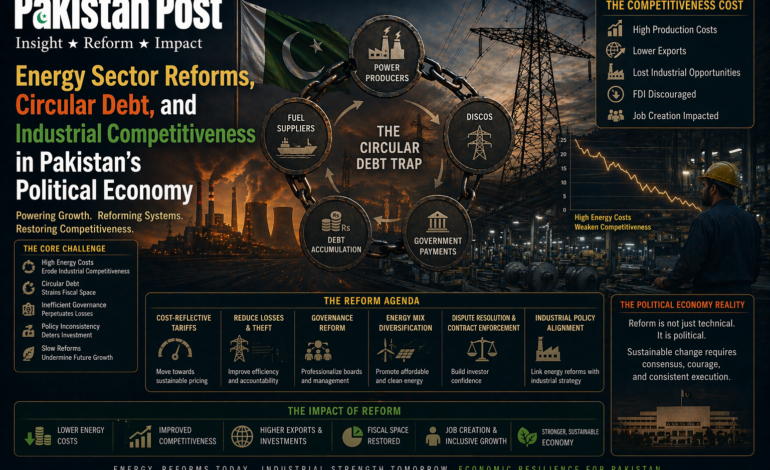

Energy sector reforms present a similar pattern of partial adjustment without structural resolution. Pakistan’s circular debt problem has persisted for over a decade, reflecting inefficiencies in distribution companies, transmission losses, tariff distortions, and political reluctance to fully pass cost-reflective pricing onto consumers. IMF programs repeatedly emphasize tariff rationalization and subsidy reduction, yet these measures are politically sensitive in an environment of high inflation and stagnant real incomes. Consequently, reforms tend to stabilize short-term cash flows without eliminating the structural drivers of debt accumulation.

The external sector adds another layer of vulnerability. Pakistan’s reliance on imported energy, limited export diversification, and relatively inelastic import demand create chronic balance-of-payments pressure. IMF programs temporarily restore external stability through exchange rate adjustments and reserve accumulation, but they do not fundamentally alter the composition of trade or the productivity base of the economy. As a result, external stabilization often proves temporary, with pressures re-emerging once capital inflows slow or global conditions tighten.

A critical dimension of this cycle is the role of exchange rate policy. Greater flexibility has been a central IMF recommendation, intended to correct overvaluation and improve export competitiveness. However, in Pakistan’s context, depreciation often feeds into inflationary pressures due to high import dependence, particularly in energy and intermediate goods. This inflationary pass-through reduces real incomes, triggers political backlash, and constrains the government’s willingness to sustain market-driven exchange rate mechanisms. The result is a managed volatility rather than a stable equilibrium.

At the institutional level, Pakistan’s reform capacity is further weakened by fragmentation across federal and provincial governance structures. Fiscal responsibilities have expanded at the subnational level following devolution, yet revenue-raising capacity remains concentrated at the federal level. This vertical imbalance complicates IMF targets, particularly those related to fiscal consolidation and public expenditure management. Coordination challenges between federal and provincial authorities often slow implementation and dilute accountability.

The political economy of reform is therefore not merely technical but deeply structural. Pakistan’s ruling governments, regardless of party affiliation, inherit a system where adjustment costs are immediate and visible, while reform benefits are delayed and diffuse. In such an environment, incentives favor short-term stabilization over long-term restructuring. IMF programs, while technically consistent, often become mechanisms for crisis management rather than transformation.

The question of whether Pakistan is trapped in cyclical dependency cannot be answered without examining the broader international financial architecture. Emerging economies with similar macroeconomic profiles often experience repeated engagement with multilateral lenders, but Pakistan’s case is distinguished by the frequency and depth of its balance-of-payments crises. The recurrence of IMF programs suggests that underlying structural constraints low productivity growth, narrow export base, weak tax capacity, and governance inefficiencies remain insufficiently addressed between stabilization cycles.

Yet it would be overly deterministic to conclude that IMF engagement is inherently counterproductive. In the absence of external financing, Pakistan would face severe external default risk, currency collapse, and deeper economic contraction. IMF programs provide critical short-term stabilization, preventing disorderly adjustment and offering a policy anchor in moments of crisis. The issue, therefore, is not the presence of IMF support, but the absence of durable domestic institutional reform that survives beyond the program lifecycle.

Recent global economic fragmentation further complicates Pakistan’s reform environment. Geoeconomic competition, supply chain realignment, and tighter global financial conditions reduce the margin for error for emerging economies. Capital is increasingly selective, favoring stable macroeconomic environments and predictable policy regimes. In this context, Pakistan’s repeated recourse to IMF programs can signal vulnerability to external investors, potentially limiting its ability to attract long-term investment beyond short-term inflows linked to stabilization episodes.

Domestic political constraints remain central to understanding why reform cycles do not translate into structural transformation. Fiscal consolidation often collides with social protection needs in an inflation-sensitive society. Energy pricing reforms face resistance due to their immediate impact on households and industry. State-owned enterprise restructuring encounters labor and political opposition. Each reform area, while economically rational in aggregate, generates concentrated losses that are politically difficult to absorb.

The absence of a sustained reform coalition across political cycles further weakens continuity. Structural reforms require multi-year commitment that extends beyond electoral mandates, yet Pakistan’s political system has struggled to maintain policy continuity across administrations. As a result, each IMF program begins in a context of partial reform fatigue, where prior commitments remain incompletely implemented or politically contested.

The deeper question is whether Pakistan’s economy is converging toward stabilization with gradual structural improvement or oscillating within a low-equilibrium trap of repeated adjustment. Evidence suggests a hybrid outcome: periodic stabilization followed by regression toward familiar vulnerabilities. External imbalances are corrected temporarily, but productivity growth remains weak; fiscal deficits are reduced temporarily, but revenue capacity remains constrained; exchange rates adjust, but export competitiveness does not significantly improve.

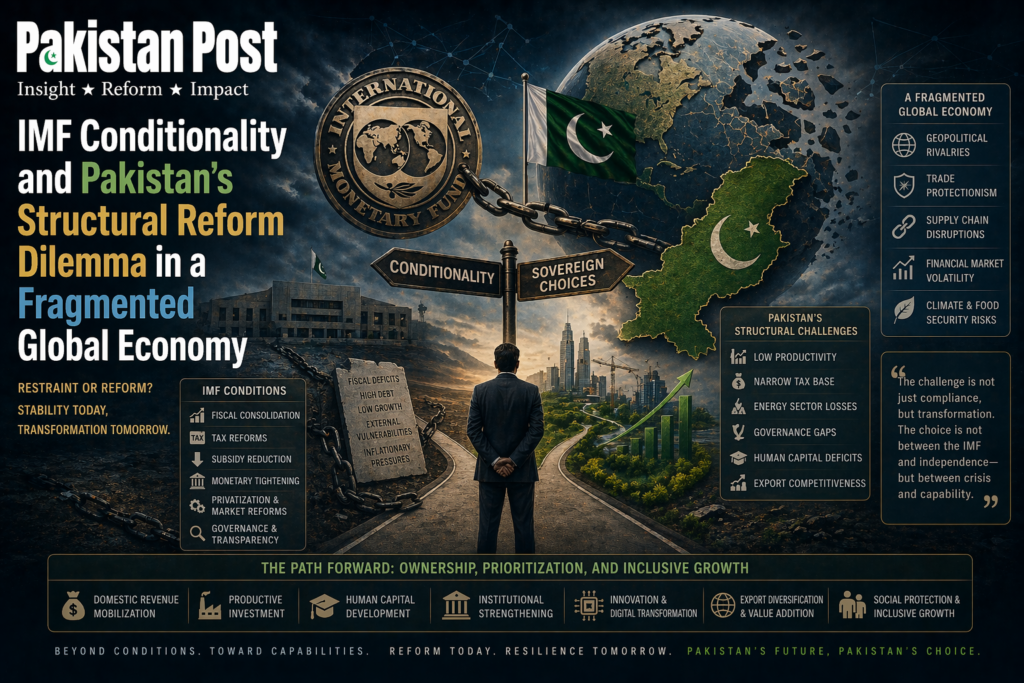

In this sense, IMF conditionality functions less as a transformation engine and more as a cyclical brake system, preventing collapse but not fundamentally altering direction. The challenge for Pakistan is to convert externally enforced discipline into internally owned reform momentum, a transition that requires institutional strengthening, political consensus, and administrative continuity.

Without such a shift, Pakistan risks remaining in a state of managed dependency, where each crisis necessitates renewed external support, and each stabilization effort postpones rather than resolves structural adjustment. The cost is not merely financial but strategic: reduced policy autonomy, constrained development planning, and persistent vulnerability to external shocks.

Ultimately, the trajectory of Pakistan’s reform process will depend on whether domestic institutions can internalize fiscal discipline, expand the tax base beyond politically sensitive sectors, restructure energy markets beyond tariff adjustments, and build an export-oriented productive economy capable of sustaining external balance. Until then, IMF programs will likely remain both a stabilizing force and a reminder of unfinished structural transformation.

A Public Service Message