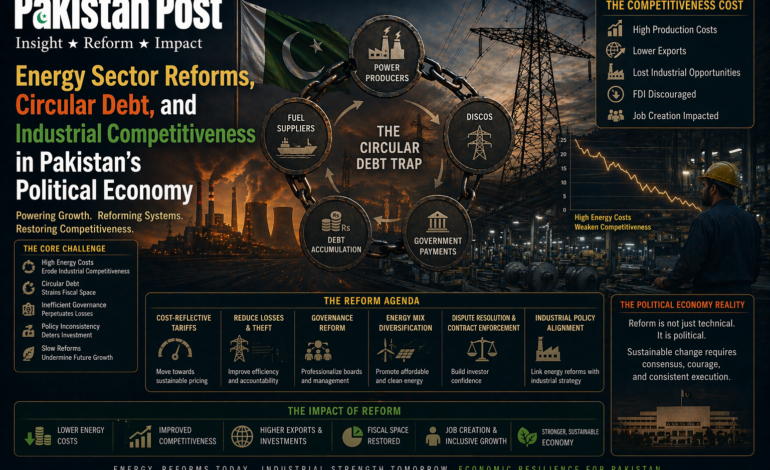

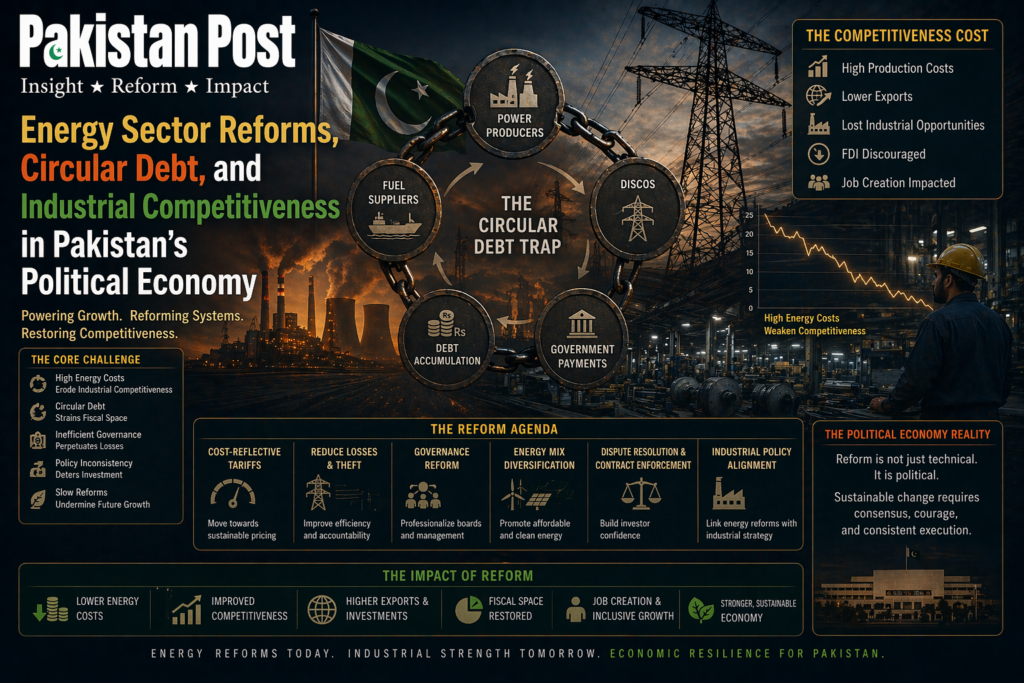

Energy Sector Reforms, Circular Debt, and Industrial Competitiveness in Pakistan’s Political Economy

Pakistan’s energy sector sits at the core of its macroeconomic instability and industrial underperformance, functioning simultaneously as a driver of fiscal stress, a constraint on export competitiveness, and a persistent source of political contestation. Over the past decade, successive governments have introduced a series of reforms aimed at addressing inefficiencies in pricing, distribution, and generation, yet the structural contradictions embedded in the sector remain largely unresolved. Instead of a clean transition toward efficiency, Pakistan’s energy landscape reflects a layered accumulation of partial fixes, where old distortions are not eliminated but redistributed across consumers, industries, and the fiscal system.

At the center of this crisis lies circular debt, a structural accumulation of unpaid obligations across the energy value chain, involving generation companies, transmission entities, distribution companies, and the government. This debt is not merely a liquidity gap but a reflection of systemic inefficiencies: transmission losses, under-recovery of tariffs, delayed subsidies, and governance weaknesses in distribution companies. Despite repeated reform commitments under IMF-supported programs and domestic policy frameworks, circular debt has continued to rise, periodically contained through fiscal injections rather than structurally eliminated.

The core tension in Pakistan’s energy reform agenda lies between economic rationality and political affordability. Cost-reflective tariffs are widely recognized as necessary for financial sustainability of the energy sector. However, in a context of high inflation, weak wage growth, and widespread energy poverty, tariff adjustments carry immediate political and social costs. Governments, therefore, often resort to delayed adjustments, cross-subsidization, and budgetary support, all of which provide short-term relief but deepen long-term structural imbalance.

This tension has significant implications for industrial competitiveness. Pakistan’s export-oriented sectors, particularly textiles, garments, and light manufacturing, operate in a regional environment where energy costs are a decisive factor in global competitiveness. Countries such as Bangladesh and Vietnam have leveraged relatively stable and predictable energy pricing to enhance industrial productivity and attract export-oriented investment. In contrast, Pakistan’s industrial base faces frequent tariff revisions, peak-load management constraints, and unreliable supply, all of which increase production costs and reduce export predictability.

Energy unreliability imposes hidden costs on industry beyond tariff levels. Firms are forced to invest in captive power generation, backup systems, and fuel storage, effectively internalizing inefficiencies that would otherwise be borne by a stable grid system. These investments divert capital away from productivity-enhancing technologies and scale expansion, locking firms into a low-productivity equilibrium. In this environment, even when nominal energy tariffs are adjusted, the effective cost of energy remains significantly higher due to inefficiency premiums embedded in the system.

Recent reforms in the energy sector have focused on tariff rationalization, subsidy reduction, and institutional restructuring of distribution companies. While these measures align with international best practices, their implementation has been uneven. Distribution companies continue to suffer from governance deficits, political interference, and weak enforcement capacity. Line losses remain structurally high in certain regions, particularly where infrastructure investment and administrative control are weak. The result is a sector that is formally restructured but operationally fragmented.

The political economy of energy reform is further complicated by intergovernmental dynamics. Following devolution and evolving fiscal arrangements, provinces and the federal government often share overlapping responsibilities in energy-related infrastructure, subsidies, and revenue allocation. This creates coordination challenges that slow reform implementation and dilute accountability. Provincial governments, facing their own political pressures, are often reluctant to enforce tariff increases or support loss-reduction measures that may be politically unpopular at the local level.

Circular debt resolution packages introduced periodically by the government provide temporary relief but fail to address root causes. These packages typically involve budgetary injections, bank borrowing, and tariff adjustments spread over time. While they stabilize liquidity in the short term, they also transfer liabilities from the energy sector to the broader fiscal system, effectively converting sectoral inefficiency into sovereign debt pressure. Over time, this dynamic increases Pakistan’s reliance on external financing, including IMF programs, to stabilize macroeconomic conditions.

The energy sector’s inefficiencies also interact with Pakistan’s broader macroeconomic constraints. High energy import dependence exposes the economy to global price volatility, particularly in oil and LNG markets. When global energy prices rise, fiscal pressure increases due to subsidy requirements and higher import bills. When prices fall, structural inefficiencies persist, as cost reductions are not fully transmitted due to delayed tariff adjustments or institutional inefficiencies. This asymmetry prevents the sector from achieving long-term equilibrium.

Industrial policy and energy policy remain insufficiently integrated. In a well-functioning growth model, energy pricing, industrial clustering, and export strategy operate in coordination. In Pakistan’s case, however, energy planning is often reactive rather than strategic, responding to fiscal constraints rather than long-term industrial priorities. As a result, energy-intensive industries face uncertainty, while potential high-value manufacturing sectors remain underdeveloped due to lack of reliable infrastructure support.

Privatization and market liberalization have been periodically proposed as solutions to structural inefficiencies in distribution and generation. However, progress has been limited due to political resistance, valuation challenges, and concerns over affordability. Partial privatization without regulatory strengthening risks creating private monopolies rather than competitive efficiency. Conversely, maintaining public ownership without governance reform perpetuates inefficiency. This policy deadlock has contributed to reform stagnation.

Technological modernization offers partial pathways for improvement, particularly in metering, grid management, and renewable integration. Pakistan’s gradual shift toward renewable energy sources, including solar and wind, has introduced new dynamics into the energy mix. However, without adequate grid modernization and storage capacity, renewable integration remains limited in its systemic impact. Moreover, net metering policies, while encouraging adoption, also create fiscal and distributional tensions within the existing tariff structure.

The broader macroeconomic implication of energy sector dysfunction is the erosion of fiscal space. Government transfers to cover losses in the energy sector reduce the capacity for public investment in education, health, and infrastructure. This crowding-out effect constrains long-term development potential and reinforces a cycle in which energy inefficiency indirectly suppresses human capital formation and productivity growth.

At the industrial level, the cumulative effect of high energy costs and unreliable supply is reduced export diversification. Pakistan remains heavily dependent on a narrow range of low- to medium-value exports, particularly textiles, limiting its integration into higher-value global supply chains. Energy instability discourages investment in sectors such as electronics, engineering goods, and advanced manufacturing, where consistent power supply and cost predictability are essential.

The key question is whether current reforms are fundamentally transforming this structure or merely managing its symptoms. Evidence suggests that while incremental improvements have been made in tariff rationalization and fiscal monitoring, the core structural drivers of inefficiency remain intact. Governance deficits in distribution companies, political sensitivity around pricing, and fragmented institutional accountability continue to constrain meaningful transformation.

Pakistan’s energy sector thus represents a classic case of reform without resolution. Each policy cycle introduces corrective measures, but the underlying political economy remains unchanged. The result is a system that periodically stabilizes under fiscal pressure but fails to evolve toward efficiency-driven sustainability.

In the absence of deeper institutional reform, Pakistan risks remaining trapped in an energy-inflation-fiscal stress loop, where energy sector inefficiencies continuously feed into macroeconomic instability and industrial underperformance. Breaking this cycle requires not only technical adjustments but a fundamental reconfiguration of incentives, governance structures, and long-term industrial alignment.

Until such alignment is achieved, energy reform in Pakistan will continue to oscillate between crisis management and partial stabilization, without reaching the level of structural transformation necessary for sustained industrial competitiveness and fiscal resilience.

A Public Service Message